Refund Arrived. Don’t Blow It.

A tax refund hitting your account can feel like free money. If you’re looking for your first car, it might be tempting to use that “free” money to get a little fancy. We would advise against that. While a tax refund can certainly help with purchasing costs, it’s not a budget. You have to consider monthly costs, which will affect what you can afford in the long run. Here’s a step-by-step guide to making sure your first car purchase is smart and gets you where you need to go.

Step 1: Plan Your Budget

Start by creating a car budget without considering your refund. This will help you stay realistic about what you can afford in monthly loan payments, as well as gas, insurance, taxes, title, registration, and maintenance costs. It’s also important to consider the overall purchase price of a car. A dealer might be able to lower your monthly payment on what seems like a good deal, but you may end up paying a much higher amount over time because of interest.

A good rule of thumb is to keep monthly car expenses under 15% of your total income. When you’re looking at how much you can afford, try to follow the 70/15/10 general budgeting rule to make sure the rest of your expenses are stable as well.

- 70% maximum for living expenses.

- 15% minimum for investments and retirement.

- 10% minimum for savings.

Step 2: Cheap to Own, Not Cheap to Buy

It’s easy to look at a low car price and think you’re getting a bargain. However, you should be careful to avoid tunnel vision. Low prices can hide problems that add up to be more expensive over time. Make sure you factor in things like vehicle history, maintenance records, number of owners, along with age and mileage.

Avoid traps like luxury brands, modified cars, listings that include “needs a little work,” and salvage or rebuilt titles. Luxury brands usually have higher repair and insurance costs compared to everyday brands. Modified cars can carry unknown quality and safety issues.

Instead, look for cars that are common, reliable, fuel-efficient, and possibly considered “boring.” Common, no-frills cars typically have lower repair and insurance costs. These all contribute to a better ownership experience for a first-time car buyer.

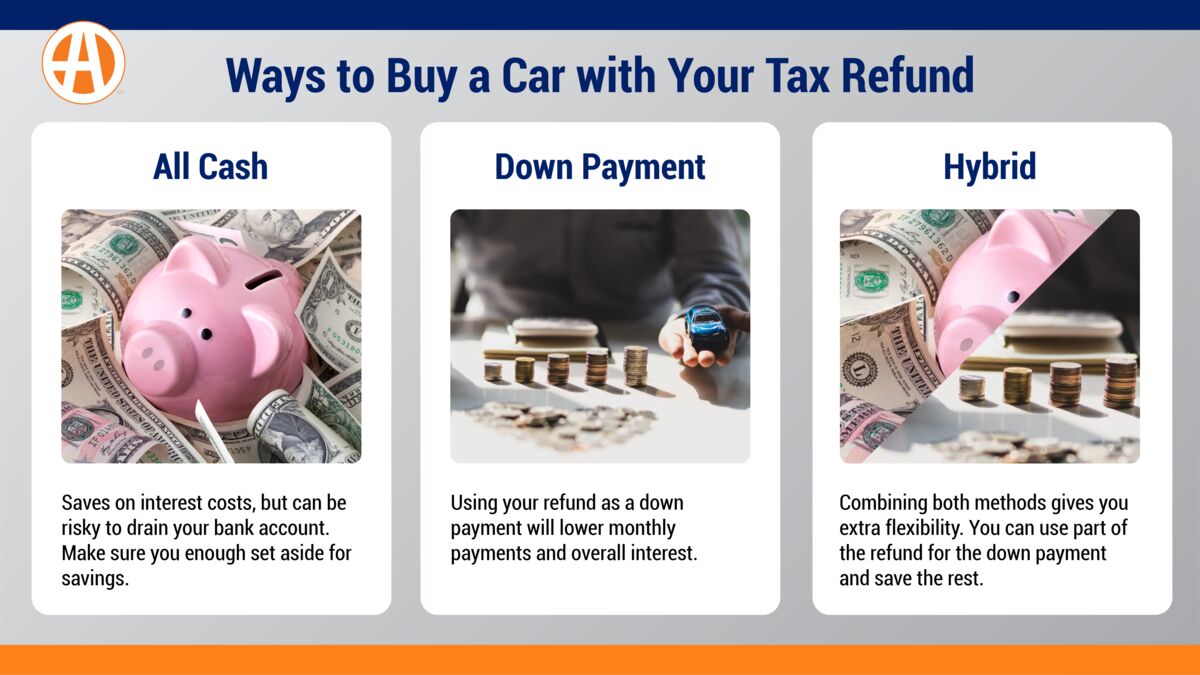

Step 3: Set a Strategy for Your Refund

Your refund can help you with your first car payment if used strategically. Look at what options work best for you.

MORE: How to Use Your Tax Refund as a Down Payment

Step 4: Shop Your Shortlist and Price Cap

Because there are so many vehicles on the market, try to narrow your search to three models that fit your needs and budget. Set your non-negotiables, such as maximum mileage, clean title only, and verifiable maintenance records. Identify your priorities.

Step 5: Go Down the Test Drive Checklist

RELATED: Test-Drive Checklist: Ensure Your Refund Car is Worth It

Step 6: Get a Pre-Purchase Inspection – It’s Insurance

A pre-purchase inspection is one of the smartest steps you can take to protect yourself. Think of it as spending a little money up front so you don’t have to spend all your money on repairs later. If a seller won’t let you get an inspection, that is a major flag, and you should not buy the car.

Once you have the inspection report, you can use the results to negotiate or know if you need to walk away.

Step 7: Close the Deal Without Getting Fee’d to Death

Here are some last things to look at before you close the deal.

Shop for Insurance Before You Buy

Insurance rates can vary by age, state, city, and model. Try to get a quote before committing to a sale to understand your costs better.

If You’re Buying From a Private Seller

Confirm that the seller actually owns the car by checking if the title is under the seller’s name. Make sure the vehicle identification number (VIN) on the paperwork matches the VIN on the car, title, and bill of sale. Keep the bill of sale for car registration and tax purposes later.

If You’re Buying From a Dealership

Dealers often try to add extra features to make more money. Feel free to decline things that you don’t need. This can include things like:

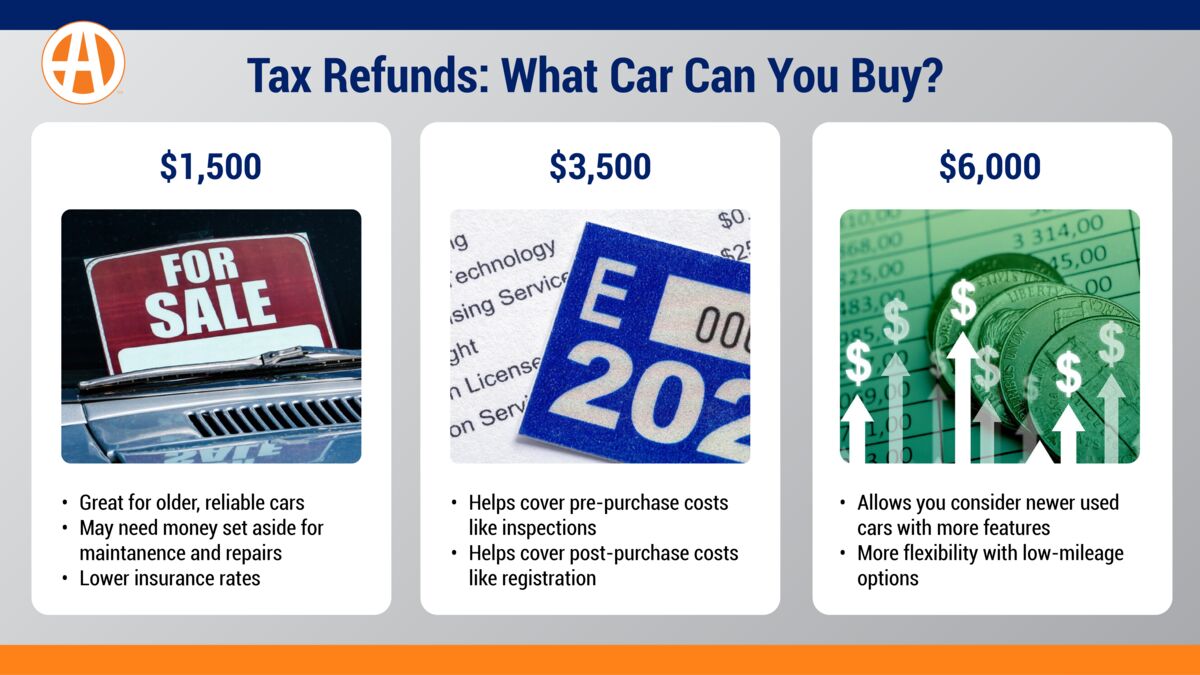

Refund Scenarios: What Can You Really Buy?

The average federal income tax refund for the 2024 tax year was $3,167, which can go a long way toward a car purchase. Whether your return is $100, $1,500, $3,500, $6,000, or more, it’s important to be realistic about how far that money can go and how best to prioritize it.

Bottom Line

If buying a car depletes your entire refund amount and savings, the car is too expensive. Make sure your first car is reliable and affordable over time, and never overextend your budget for an automobile. You can always upgrade your vehicle when you have more money in the bank.