According to Cox Automotive’s 2026 Forecast, an estimated 2.9 million vehicles will be leased in 2026. Lease penetration is projected to be 2% less than 2025, reflecting overall trends of decreased car sales. Some drivers may opt for this short-term arrangement in favor of lower monthly payments, but knowing the ins and outs of leasing is critical to understanding if it’s a good deal. So, should you lease a car?

How Does Car Leasing Work?

A car lease is an agreement that gives the consumer the right to use the leased vehicle over a set period. Instead of outright ownership, car leasing works more like a long-term rental where the driver doesn’t own the vehicle but is still responsible its use. Leases are subject to term limits, usually two or three years. One-year car leases are uncommon, so if you need a shorter term, a longer-term car rental may be a better option. Car leases also include mileage limits where lessees are charged when they exceed the mileage cap.

The monthly payment is determined by several factors, including the vehicle’s depreciation, the number of miles put on the vehicle, and its condition at the end of the lease. Monthly lease payments also include the cost of financing the transaction. A monthly lease payment is usually lower than a loan installment. Automakers will sometimes offer special lease deals that add discounts on top of the monthly lease price.

Can You Lease a Used Car?

Some programs allow you to lease a Certified Preowned car.

When Does Leasing Make Sense?

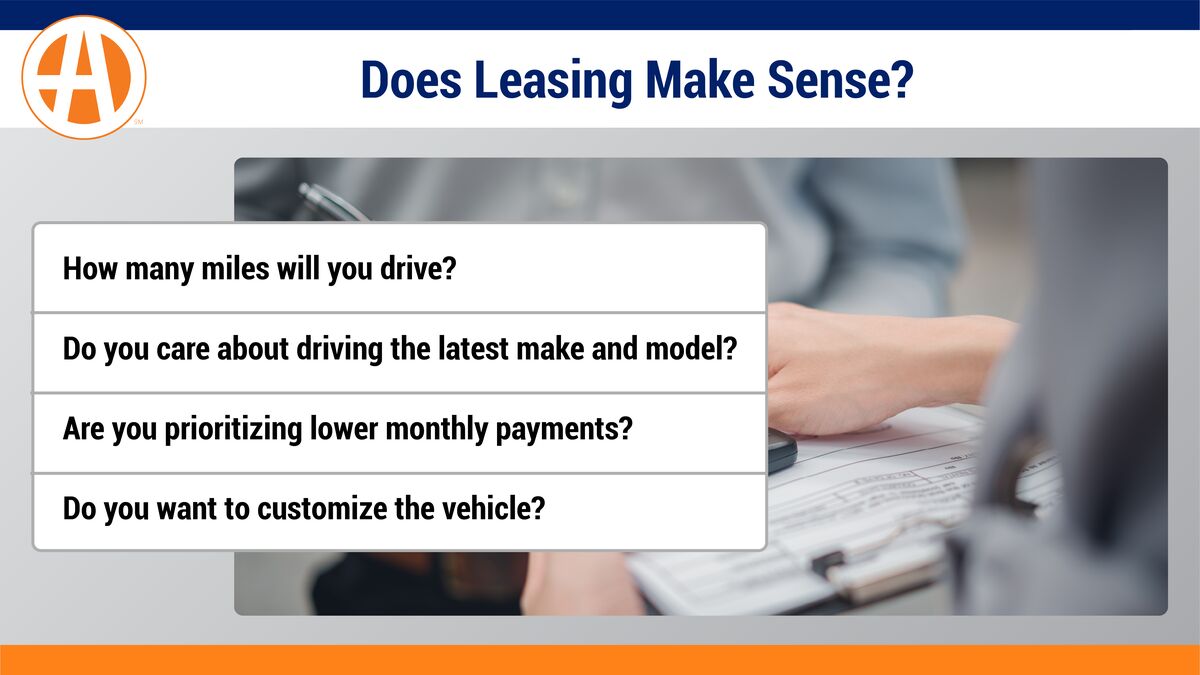

Leasing is a good option for many people, but it’s not the best choice for everyone. Here are the main factors to consider when deciding to lease a car:

- How many miles will you drive? If you’re taking frequent road trips or anticipate running lots of errands around town, the mileage limits associated with lease contracts may not be a good fit for you.

- Do you care about driving the latest make and model? If so, you may prefer the lower level of commitment associated with a short-term lease.

- Are you prioritizing lower monthly payments? A lease may be the right option if you are looking for a lower car payment. Still, it is important to evaluate the long-term costs associated with leasing a vehicle, including fees and penalties.

- Do you want to customize the vehicle? If you want the freedom and flexibility to make modifications and personal upgrades, a lease is not a good idea.

RELATED: Lease vs. Finance a Car: 5 Things to Consider

Car Leasing Pros and Cons

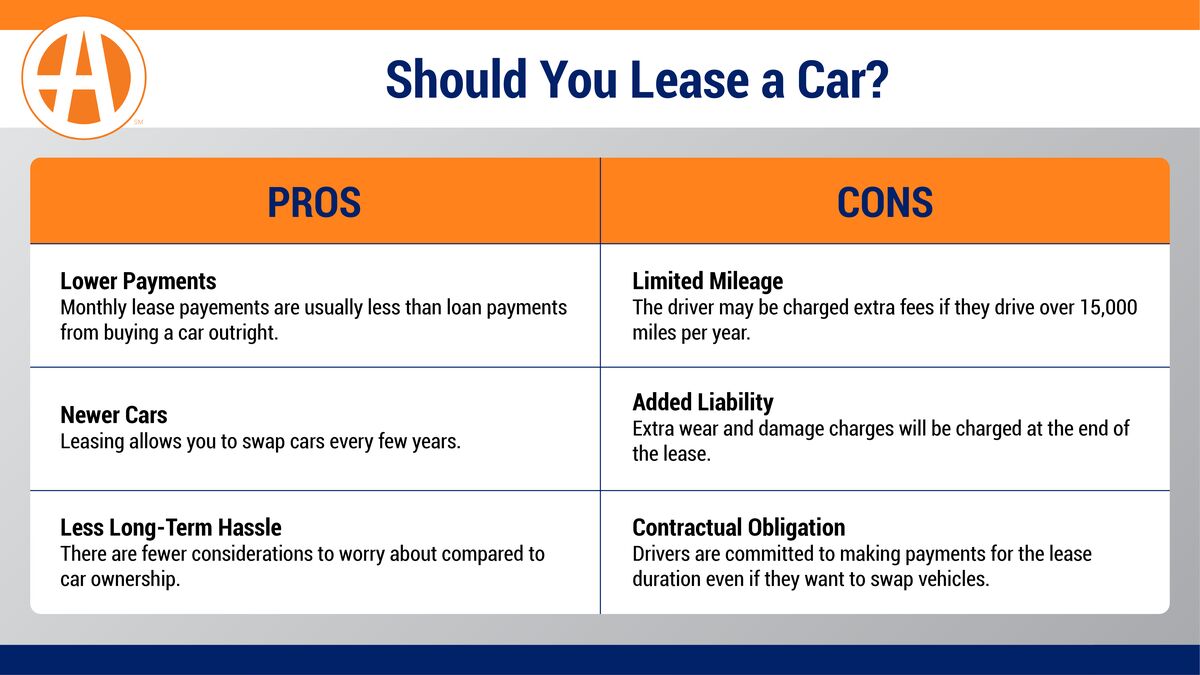

So when is car leasing worth it? Leasing a car can make more sense under specific circumstances. You’ll want to consider factors like mileage and car models. If you put fewer than 15,000 miles on your car per year, leasing might be a good option. Others may opt for leasing because they like driving newer car models and want to switch every few years. Plus, lower monthly lease payments allow you to drive a more expensive vehicle with more advanced technologies and features. There are a few key benefits and drawbacks to leasing.

Pros

- Lower Payments: Prices of new vehicles continue to climb each year as manufacturers add new features and technology. Leasing allows you to keep your car payment in check. Keep an eye out for incentives and rebates, which may be more generous than traditional cash buyers’ discounts or low-interest-rate offers.

- Newer Cars: If you want to drive a new car, leasing is the way to go since most range from two to four years in duration. If you buy a vehicle outright, you’ll likely keep it for much longer.

- Less Long-Term Hassle: Since you have no stake in the vehicle, leasing offers the advantage of not having to worry about what to do with the vehicle when you want a new one. The shorter lease term also means your car will likely be covered by the manufacturer’s warranty the entire time you keep the vehicle. Not so with a buyer who may still be paying down their loan long after the warranty has expired.

Cons

- Limited Mileage: If you drive a lot, you may find it more cost-effective to buy and keep the car. Most leases cap mileage at 10,000 to 15,000 miles per year. You might find yourself paying thousands of dollars more if you go over the cap, as fees can range as high as 25 cents per mile.

- Added Liability: In addition to mileage, the lessee must cover any damage or excess wear and tear on the car. Most scratches and dings are considered normal wear and tear, but read the fine print to determine what excess wear and tear looks like and for what and how much you are liable.

- Contractual Obligation: Remember that a lease is a contract, and you’re committed to making the payments for the duration. If you decide you want out, you may still be liable for the balance of your payments. Be sure to check the lease to determine your liability carefully.

How to Tell if a Car Lease Is a Good Deal

Use Autotrader’s Lease Calculator to help estimate how much it costs to lease a car. Remember to factor in all charges like down payments, disposal fees, and acquisition fees. All these payments, including taxes, licenses, and registration fees, should be divided by the term and added to your monthly payment to determine your actual out-of-pocket costs.

For a good deal on a lease payment, expect to pay 1% of a new vehicle’s price each month. Following this rule, a new vehicle with a price of $49,000 would be $490 per month.

Other Payment Considerations

Three fundamental factors make up a lease: how much it costs to acquire the vehicle, the interest charged to cover the financing, and what the car will be worth at the end of the lease.

The most significant component is what’s known as the capitalized cost. That’s the amount the lessor pays for the vehicle, and is usually at or below the Manufacturer’s Suggested Retail Price (MSRP). This has a direct effect on your monthly payment.

Any additional funds, such as down payments or incentives, also reduce the vehicle’s capitalized cost. Another critical factor is the residual or resale value of the vehicle assigned to the deal. A high residual lowers the capitalized cost and lowers the payments. A low residual raises that cost and the monthlies. Review all these figures before signing the lease agreement, especially the residual value.

What to Expect at the End of a Lease

Traditional leases come in open- and closed-end contracts. Typically, a closed-end lease will cost more than an open-end contract because of the higher risks and costs for the lessor. Closed-end leases are also known as walkaway leases, where the lessee has no responsibility outside of excess mileage or wear. In this case, the lessor is also responsible for the vehicle’s disposal. With open-end leases, there is a lease buyback option at the end.

READ MORE: End of Lease — What You Need to Know

Editor’s Note: We have updated this article since its initial publication. Colin Ryan contributed to this report.